NumPy-версия "Экспоненциально-взвешенного скользящего среднего", эквивалентная pandas.ewm(). Mean()

Как мне получить экспоненциально-взвешенное скользящее среднее в NumPy, как в пандах?

import pandas as pd

import pandas_datareader as pdr

from datetime import datetime

# Declare variables

ibm = pdr.get_data_yahoo(symbols='IBM', start=datetime(2000, 1, 1), end=datetime(2012, 1, 1)).reset_index(drop=True)['Adj Close']

windowSize = 20

# Get PANDAS exponential weighted moving average

ewm_pd = pd.DataFrame(ibm).ewm(span=windowSize, min_periods=windowSize).mean().as_matrix()

print(ewm_pd)

Я попробовал следующее с NumPy

import numpy as np

import pandas_datareader as pdr

from datetime import datetime

# From this post: http://stackru.com/a/40085052/3293881 by @Divakar

def strided_app(a, L, S): # Window len = L, Stride len/stepsize = S

nrows = ((a.size - L) // S) + 1

n = a.strides[0]

return np.lib.stride_tricks.as_strided(a, shape=(nrows, L), strides=(S * n, n))

def numpyEWMA(price, windowSize):

weights = np.exp(np.linspace(-1., 0., windowSize))

weights /= weights.sum()

a2D = strided_app(price, windowSize, 1)

returnArray = np.empty((price.shape[0]))

returnArray.fill(np.nan)

for index in (range(a2D.shape[0])):

returnArray[index + windowSize-1] = np.convolve(weights, a2D[index])[windowSize - 1:-windowSize + 1]

return np.reshape(returnArray, (-1, 1))

# Declare variables

ibm = pdr.get_data_yahoo(symbols='IBM', start=datetime(2000, 1, 1), end=datetime(2012, 1, 1)).reset_index(drop=True)['Adj Close']

windowSize = 20

# Get NumPy exponential weighted moving average

ewma_np = numpyEWMA(ibm, windowSize)

print(ewma_np)

Но результаты не такие, как у панд.

Возможно, есть лучший подход для вычисления экспоненциально-взвешенной скользящей средней непосредственно в NumPy и получения того же результата, что и pandas.ewm().mean()?

На 60 000 запросов на решение панд я получаю около 230 секунд. Я уверен, что с чистым NumPy это может быть значительно уменьшено.

15 ответов

Я думаю, что я наконец взломал это!

Вот векторизованная версия numpy_ewma функция, которая, как утверждается, дает правильные результаты @RaduS's post -

def numpy_ewma_vectorized(data, window):

alpha = 2 /(window + 1.0)

alpha_rev = 1-alpha

scale = 1/alpha_rev

n = data.shape[0]

r = np.arange(n)

scale_arr = scale**r

offset = data[0]*alpha_rev**(r+1)

pw0 = alpha*alpha_rev**(n-1)

mult = data*pw0*scale_arr

cumsums = mult.cumsum()

out = offset + cumsums*scale_arr[::-1]

return out

Дальнейшее повышение

Мы можем повысить его еще раз с помощью некоторого повторного использования кода, например:

def numpy_ewma_vectorized_v2(data, window):

alpha = 2 /(window + 1.0)

alpha_rev = 1-alpha

n = data.shape[0]

pows = alpha_rev**(np.arange(n+1))

scale_arr = 1/pows[:-1]

offset = data[0]*pows[1:]

pw0 = alpha*alpha_rev**(n-1)

mult = data*pw0*scale_arr

cumsums = mult.cumsum()

out = offset + cumsums*scale_arr[::-1]

return out

Испытание во время выполнения

Давайте сопоставим эти два с одной и той же цикличной функцией для большого набора данных.

In [97]: data = np.random.randint(2,9,(5000))

...: window = 20

...:

In [98]: np.allclose(numpy_ewma(data, window), numpy_ewma_vectorized(data, window))

Out[98]: True

In [99]: np.allclose(numpy_ewma(data, window), numpy_ewma_vectorized_v2(data, window))

Out[99]: True

In [100]: %timeit numpy_ewma(data, window)

100 loops, best of 3: 6.03 ms per loop

In [101]: %timeit numpy_ewma_vectorized(data, window)

1000 loops, best of 3: 665 µs per loop

In [102]: %timeit numpy_ewma_vectorized_v2(data, window)

1000 loops, best of 3: 357 µs per loop

In [103]: 6030/357.0

Out[103]: 16.89075630252101

Ускорение в 17 раз!

Обновлено 27/11/2018

РАБОТАЯ ЧИСТАЯ ЧИСТОТА, БЫСТРОЕ И ВЕКТОРИЗОВАННОЕ РЕШЕНИЕ ДЛЯ БОЛЬШИХ ВХОДОВ

параметр out для вычисления на месте, параметр dtype, параметр порядка индекса

Ответ Дивакара приводит к проблемам с точностью с плавающей запятой, когда ввод слишком велик. Это потому что (1-alpha)**(n+1) -> 0 когда n -> inf а также alpha -> 1, что приводит к делению на ноль и NaN значения выскакивают в расчете.

Вот мое самое быстрое решение без проблем точности, почти полностью векторизованное. Это стало немного сложнее, но производительность отличная, особенно для действительно огромных входов. Без использования вычислений на месте (что возможно при использовании out параметр, экономящий время выделения памяти): 3,62 секунды для входного вектора элемента 100 М, 3,2 мс для вектора входа элемента 100 К и 293 мкс для вектора входа 5000 элементов на довольно старом ПК (результаты могут отличаться в зависимости от alpha/row_size ценности).

# tested with python3 & numpy 1.15.2

import numpy as np

def ewma_vectorized_safe(data, alpha, row_size=None, dtype=None, order='C', out=None):

"""

Reshapes data before calculating EWMA, then iterates once over the rows

to calculate the offset without precision issues

:param data: Input data, will be flattened.

:param alpha: scalar float in range (0,1)

The alpha parameter for the moving average.

:param row_size: int, optional

The row size to use in the computation. High row sizes need higher precision,

low values will impact performance. The optimal value depends on the

platform and the alpha being used. Higher alpha values require lower

row size.

:param dtype: optional

Data type used for calculations. Defaults to float64 unless

data.dtype is float32, then it will use float32.

:param order: {'C', 'F', 'A'}, optional

Order to use when flattening the data. Defaults to 'C'.

:param out: ndarray, or None, optional

A location into which the result is stored. If provided, it must have

the same shape as the desired output. If not provided or `None`,

a freshly-allocated array is returned.

:return: The flattened result.

"""

if dtype is None:

if data.dtype == np.float32:

dtype = np.float32

else:

dtype = np.float64

else:

dtype = np.dtype(dtype)

row_size = int(row_size) if row_size is not None

else get_max_row_size(alpha, dtype)

data = np.array(data, copy=False)

if data.size <= row_size:

# The normal function can handle this input, use that

return ewma_vectorized(data, alpha, dtype=dtype, order=order, out=out)

if data.ndim > 1:

# flatten input

data = np.reshape(data, -1, order=order)

if out is None:

out = np.empty_like(data, dtype=dtype)

else:

assert out.shape == data.shape

assert out.dtype == dtype

row_n = int(data.size // row_size) # the number of rows to use

trailing_n = int(data.size % row_size) # the amount of data leftover

first_offset = data[0]

if trailing_n > 0:

# set temporary results to slice view of out parameter

out_main_view = np.reshape(out[:-trailing_n], (row_n, row_size))

data_main_view = np.reshape(data[:-trailing_n], (row_n, row_size))

else:

out_main_view = out

data_main_view = data

# get all the scaled cumulative sums with 0 offset

ewma_vectorized_2d(data_main_view, alpha, axis=1, offset=0, dtype=dtype,

order='C', out=out_main_view)

scaling_factors = (1 - alpha) ** (np.arange(1, row_size + 1, dtype=dtype))

last_scaling_factor = scaling_factors[-1]

# create offset array

offsets = np.empty(out_main_view.shape[0], dtype=dtype)

offsets[0] = first_offset

# iteratively calculate offset for each row

for i in range(1, out_main_view.shape[0]):

offsets[i] = offsets[i - 1] * last_scaling_factor + out_main_view[i - 1, -1]

# add the offsets to the result

out_main_view += offsets[:, np.newaxis] * scaling_factors[np.newaxis, :]

if trailing_n > 0:

# process trailing data in the 2nd slice of the out parameter

ewma_vectorized(data[-trailing_n:], alpha, offset=out_main_view[-1, -1],

dtype=dtype, order='C', out=out[-trailing_n:])

return out

def get_max_row_size(alpha, dtype=float):

assert 0. <= alpha < 1.

# This will return the maximum row size possible on

# your platform for the given dtype. I can find no impact on accuracy

# at this value on my machine.

# Might not be the optimal value for speed, which is hard to predict

# due to numpy's optimizations

# Use np.finfo(dtype).eps if you are worried about accuracy

# and want to be extra safe.

epsilon = np.finfo(dtype).tiny

# If this produces an OverflowError, make epsilon larger

return int(np.log(epsilon)/np.log(1-alpha)) + 1

Функция 1D EWMA:

def ewma_vectorized(data, alpha, offset=None, dtype=None, order='C', out=None):

"""

Calculates the exponential moving average over a vector.

Will fail for large inputs.

:param data: Input data

:param alpha: scalar float in range (0,1)

The alpha parameter for the moving average.

:param offset: optional

The offset for the moving average, scalar. Defaults to data[0].

:param dtype: optional

Data type used for calculations. Defaults to float64 unless

data.dtype is float32, then it will use float32.

:param order: {'C', 'F', 'A'}, optional

Order to use when flattening the data. Defaults to 'C'.

:param out: ndarray, or None, optional

A location into which the result is stored. If provided, it must have

the same shape as the input. If not provided or `None`,

a freshly-allocated array is returned.

"""

if dtype is None:

if data.dtype == np.float32:

dtype = np.float32

else:

dtype = np.float64

else:

dtype = np.dtype(dtype)

data = np.array(data, copy=False)

if data.ndim > 1:

# flatten input

data = data.reshape(-1, order)

if out is None:

out = np.empty_like(data, dtype=dtype)

else:

assert out.shape == data.shape

assert out.dtype == dtype

if data.size < 1:

# empty input, return empty array

return out

if offset is None:

offset = data[0]

alpha = np.array(alpha, copy=False).astype(dtype, copy=False)

# scaling_factors -> 0 as len(data) gets large

# this leads to divide-by-zeros below

scaling_factors = np.power(1. - alpha, np.arange(row_size + 1, dtype=dtype),

dtype=dtype)

# create cumulative sum array

np.multiply(data, (alpha * scaling_factors[-2]) / scaling_factors[:-1],

dtype=dtype, out=out)

np.cumsum(out, dtype=dtype, out=out)

# cumsums / scaling

out /= scaling_factors[-2::-1]

if offset != 0:

offset = np.array(offset, copy=False).astype(dtype, copy=False)

# add offsets

out += offset * scaling_factors[1:]

return out

Функция 2D EWMA:

def ewma_vectorized_2d(data, alpha, axis=None, offset=None, dtype=None, order='C', out=None):

"""

Calculates the exponential moving average over a given axis.

:param data: Input data, must be 1D or 2D array.

:param alpha: scalar float in range (0,1)

The alpha parameter for the moving average.

:param axis: The axis to apply the moving average on.

If axis==None, the data is flattened.

:param offset: optional

The offset for the moving average. Must be scalar or a

vector with one element for each row of data. If set to None,

defaults to the first value of each row.

:param dtype: optional

Data type used for calculations. Defaults to float64 unless

data.dtype is float32, then it will use float32.

:param order: {'C', 'F', 'A'}, optional

Order to use when flattening the data. Ignored if axis is not None.

:param out: ndarray, or None, optional

A location into which the result is stored. If provided, it must have

the same shape as the desired output. If not provided or `None`,

a freshly-allocated array is returned.

"""

data = np.array(data, copy=False)

assert data.ndim <= 2

if dtype is None:

if data.dtype == np.float32:

dtype = np.float32

else:

dtype = np.float64

else:

dtype = np.dtype(dtype)

if out is None:

out = np.empty_like(data, dtype=dtype)

else:

assert out.shape == data.shape

assert out.dtype == dtype

if data.size < 1:

# empty input, return empty array

return out

if axis is None or data.ndim < 2:

# use 1D version

if isinstance(offset, np.ndarray):

offset = offset[0]

return ewma_vectorized(data, alpha, offset, dtype=dtype, order=order,

out=out)

assert -data.ndim <= axis < data.ndim

# create reshaped data views

out_view = out

if axis < 0:

axis = data.ndim - int(axis)

if axis == 0:

# transpose data views so columns are treated as rows

data = data.T

out_view = data.T

if offset is None:

# use the first element of each row as the offset

offset = np.copy(data[:, 0])

elif np.size(offset) == 1:

offset = np.reshape(offset, (1,))

alpha = np.array(alpha, copy=False).astype(dtype, copy=False)

# calculate the moving average

row_size = data.shape[1]

row_n = data.shape[0]

scaling_factors = np.power(1. - alpha, np.arange(row_size + 1, dtype=dtype),

dtype=dtype)

# create a scaled cumulative sum array

np.multiply(

data,

np.multiply(alpha * scaling_factors[-2], np.ones((row_n, 1), dtype=dtype),

dtype=dtype)

/ scaling_factors[np.newaxis, :-1],

dtype=dtype, out=out_view

)

np.cumsum(out_view, axis=1, dtype=dtype, out=out_view)

out_view /= scaling_factors[np.newaxis, -2::-1]

if not (np.size(offset) == 1 and offset == 0):

offset = offset.astype(dtype, copy=False)

# add the offsets to the scaled cumulative sums

out_view += offset[:, np.newaxis] * scaling_factors[np.newaxis, 1:]

return out

использование:

data_n = 100000000

data = ((0.5*np.random.randn(data_n)+0.5) % 1) * 100

window = 5000

sum_proportion = .875

alpha = 1 - np.exp(np.log(1 - sum_proportion) / window) # or 2/(window+1) for panda's span function

result = ewma_vectorized_safe(data, alpha)

Просто совет

Легко вычислить "размер окна" (технически экспоненциальные средние имеют бесконечные "окна") для данного alphaв зависимости от вклада данных в этом окне в среднее значение. Это полезно, например, для выбора того, какую часть начала результата следует рассматривать как ненадежную из-за граничных эффектов.

sum_proportion = .99 # window covers 99% of contribution to the moving average

scale_factors = (1 - alpha) ** (np.arange(data.shape[0] + 1))

scale_factor_cumsum = np.cumsum(scale_factors)

# window_size is the index of the first partial sum of scale_factors

# where partial_sum > sum_proportion * total_sum.

# Increases with increased sum_proportion and decreased alpha

window_size = np.argmax(scale_factor_cumsum > sum_proportion * scale_factor_cumsum[-1])

или более математически, но эффективно:

def window_size(alpha, sum_proportion):

# solve (1-alpha)**window_size = (1-sum_proportion) for window_size

return int(np.log(1-sum_proportion) / np.log(1-alpha))

alpha = 2 / (window_size + 1.0) Отношение, используемое в этой теме (опция 'span' от pandas), является очень грубым приближением обратной функции выше (с sum_proportion~=0.87). alpha = 1 - np.exp(np.log(1-sum_proportion)/window_size) является более точным (опция "период полураспада" от панд равна этой формуле sum_proportion=0.5).

В следующем примере data представляет непрерывный шумовой сигнал. cutoff_idx это первая позиция в result где по крайней мере 99% значения зависит от отдельных значений в data (т.е. менее 1% зависит от данных [0]). Данные до cutoff_idx исключен из окончательных результатов, поскольку он слишком зависит от первого значения в dataпоэтому возможно искажение среднего.

result = ewma_vectorized_safe(data, alpha, chunk_size)

sum_proportion = .99

cutoff_idx = window_size(alpha, sum_proportion)

result = result[cutoff_idx:]

Чтобы проиллюстрировать проблему, описанную выше, вы можете запустить ее несколько раз, обратите внимание на часто появляющийся фальстарт красной линии, который пропускается после cutoff_idx:

data_n = 100000

data = np.random.rand(data_n) * 100

window = 1000

chunk_size = 10000

sum_proportion = .99

alpha = 1 - np.exp(np.log(1-sum_proportion)/window)

result = ewma_vectorized_safe(data, alpha, chunk_size)

cutoff_idx = window_size(alpha, sum_proportion)

x = np.arange(start=0, stop=result.size)

import matplotlib.pyplot as plt

plt.plot(x[:cutoff_idx+1], result[:cutoff_idx+1], '-r',

x[cutoff_idx:], result[cutoff_idx:], '-b')

plt.show()

Обратите внимание, что cutoff_idx==window потому что альфа была установлена с обратной window_size() функция, с тем же sum_proportion,

Самый быстрый EWMA 23x pandas

Вопрос строго задает numpy Решение, однако, кажется, что ОП был на самом деле только после чистого numpy решение для ускорения времени выполнения.

Я решил похожую проблему, но вместо этого посмотрел в сторону numba.jit что значительно ускоряет время вычислений

In [24]: a = np.random.random(10**7)

...: df = pd.Series(a)

In [25]: %timeit numpy_ewma(a, 10) # /a/42915307/4013571

...: %timeit df.ewm(span=10).mean() # pandas

...: %timeit numpy_ewma_vectorized_v2(a, 10) # best w/o numba: /a/42926270/4013571

...: %timeit _ewma(a, 10) # fastest accurate (below)

...: %timeit _ewma_infinite_hist(a, 10) # fastest overall (below)

4.14 s ± 116 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

991 ms ± 52.2 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

396 ms ± 8.39 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

181 ms ± 1.01 ms per loop (mean ± std. dev. of 7 runs, 10 loops each)

39.6 ms ± 979 µs per loop (mean ± std. dev. of 7 runs, 10 loops each)

Сокращение до меньших массивов a = np.random.random(100) (результаты в том же порядке)

41.6 µs ± 491 ns per loop (mean ± std. dev. of 7 runs, 10000 loops each)

945 ms ± 12 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

16 µs ± 93.5 ns per loop (mean ± std. dev. of 7 runs, 100000 loops each)

1.66 µs ± 13.7 ns per loop (mean ± std. dev. of 7 runs, 1000000 loops each)

1.14 µs ± 5.57 ns per loop (mean ± std. dev. of 7 runs, 1000000 loops each)

Также стоит отметить, что мои функции, приведенные ниже, идентичны pandas (см. примеры в docstr), в то время как некоторые ответы здесь имеют различные приближения. Например,

In [57]: print(pd.DataFrame([1,2,3]).ewm(span=2).mean().values.ravel())

...: print(numpy_ewma_vectorized_v2(np.array([1,2,3]), 2))

...: print(numpy_ewma(np.array([1,2,3]), 2))

[1. 1.75 2.61538462]

[1. 1.66666667 2.55555556]

[1. 1.18181818 1.51239669]

Исходный код, который я задокументировал для моей собственной библиотеки

import numpy as np

from numba import jit

from numba import float64

from numba import int64

@jit((float64[:], int64), nopython=True, nogil=True)

def _ewma(arr_in, window):

r"""Exponentialy weighted moving average specified by a decay ``window``

to provide better adjustments for small windows via:

y[t] = (x[t] + (1-a)*x[t-1] + (1-a)^2*x[t-2] + ... + (1-a)^n*x[t-n]) /

(1 + (1-a) + (1-a)^2 + ... + (1-a)^n).

Parameters

----------

arr_in : np.ndarray, float64

A single dimenisional numpy array

window : int64

The decay window, or 'span'

Returns

-------

np.ndarray

The EWMA vector, same length / shape as ``arr_in``

Examples

--------

>>> import pandas as pd

>>> a = np.arange(5, dtype=float)

>>> exp = pd.DataFrame(a).ewm(span=10, adjust=True).mean()

>>> np.array_equal(_ewma_infinite_hist(a, 10), exp.values.ravel())

True

"""

n = arr_in.shape[0]

ewma = np.empty(n, dtype=float64)

alpha = 2 / float(window + 1)

w = 1

ewma_old = arr_in[0]

ewma[0] = ewma_old

for i in range(1, n):

w += (1-alpha)**i

ewma_old = ewma_old*(1-alpha) + arr_in[i]

ewma[i] = ewma_old / w

return ewma

@jit((float64[:], int64), nopython=True, nogil=True)

def _ewma_infinite_hist(arr_in, window):

r"""Exponentialy weighted moving average specified by a decay ``window``

assuming infinite history via the recursive form:

(2) (i) y[0] = x[0]; and

(ii) y[t] = a*x[t] + (1-a)*y[t-1] for t>0.

This method is less accurate that ``_ewma`` but

much faster:

In [1]: import numpy as np, bars

...: arr = np.random.random(100000)

...: %timeit bars._ewma(arr, 10)

...: %timeit bars._ewma_infinite_hist(arr, 10)

3.74 ms ± 60.2 µs per loop (mean ± std. dev. of 7 runs, 100 loops each)

262 µs ± 1.54 µs per loop (mean ± std. dev. of 7 runs, 1000 loops each)

Parameters

----------

arr_in : np.ndarray, float64

A single dimenisional numpy array

window : int64

The decay window, or 'span'

Returns

-------

np.ndarray

The EWMA vector, same length / shape as ``arr_in``

Examples

--------

>>> import pandas as pd

>>> a = np.arange(5, dtype=float)

>>> exp = pd.DataFrame(a).ewm(span=10, adjust=False).mean()

>>> np.array_equal(_ewma_infinite_hist(a, 10), exp.values.ravel())

True

"""

n = arr_in.shape[0]

ewma = np.empty(n, dtype=float64)

alpha = 2 / float(window + 1)

ewma[0] = arr_in[0]

for i in range(1, n):

ewma[i] = arr_in[i] * alpha + ewma[i-1] * (1 - alpha)

return ewma

Вот реализация, использующая NumPy, которая эквивалентна использованию df.ewm(alpha=alpha).mean(), После прочтения документации, это всего лишь несколько матричных операций. Хитрость заключается в построении правильных матриц.

Стоит отметить, что, поскольку мы создаем матрицы с плавающей точкой, вы можете быстро перебрать вашу память, если входной массив слишком велик.

import pandas as pd

import numpy as np

def ewma(x, alpha):

'''

Returns the exponentially weighted moving average of x.

Parameters:

-----------

x : array-like

alpha : float {0 <= alpha <= 1}

Returns:

--------

ewma: numpy array

the exponentially weighted moving average

'''

# Coerce x to an array

x = np.array(x)

n = x.size

# Create an initial weight matrix of (1-alpha), and a matrix of powers

# to raise the weights by

w0 = np.ones(shape=(n,n)) * (1-alpha)

p = np.vstack([np.arange(i,i-n,-1) for i in range(n)])

# Create the weight matrix

w = np.tril(w0**p,0)

# Calculate the ewma

return np.dot(w, x[::np.newaxis]) / w.sum(axis=1)

Давайте проверим его:

alpha = 0.55

x = np.random.randint(0,30,15)

df = pd.DataFrame(x, columns=['A'])

df.ewm(alpha=alpha).mean()

# returns:

# A

# 0 13.000000

# 1 22.655172

# 2 20.443268

# 3 12.159796

# 4 14.871955

# 5 15.497575

# 6 20.743511

# 7 20.884818

# 8 24.250715

# 9 18.610901

# 10 17.174686

# 11 16.528564

# 12 17.337879

# 13 7.801912

# 14 12.310889

ewma(x=x, alpha=alpha)

# returns:

# array([ 13. , 22.65517241, 20.44326778, 12.1597964 ,

# 14.87195534, 15.4975749 , 20.74351117, 20.88481763,

# 24.25071484, 18.61090129, 17.17468551, 16.52856393,

# 17.33787888, 7.80191235, 12.31088889])

Очень простое решение, позволяющее избежать numba, но почти такое же быстрое, как решение Александра Макфарлейна, особенно для больших массивов и больших массивов.window размеры, это использовать scipy's lfilter функция (поскольку EWMA является линейным фильтром):

from scipy.signal import lfiltic, lfilter

# careful not to mix between scipy.signal and standard python signal

# (https://docs.python.org/3/library/signal.html) if your code handles some processes

def ewma_linear_filter(array, window):

alpha = 2 /(window + 1)

b = [alpha]

a = [1, alpha-1]

zi = lfiltic(b, a, array[0:1], [0])

return lfilter(b, a, array, zi=zi)[0]

Сроки следующие:

n = 10_000_000

window = 100_000

data = np.random.normal(0, 1, n)

%timeit _ewma_infinite_hist(data, window)

%timeit linear_filter(data, window)

86 ms ± 1.1 ms per loop (mean ± std. dev. of 7 runs, 10 loops each)

92.6 ms ± 751 µs per loop (mean ± std. dev. of 7 runs, 10 loops each)

Этот ответ может показаться неуместным. Но для тех, кому также необходимо рассчитать экспоненциально взвешенную дисперсию (а также стандартное отклонение) с помощью NumPy, будет полезно следующее решение:

import numpy as np

def ew(a, alpha, winSize):

_alpha = 1 - alpha

ws = _alpha ** np.arange(winSize)

w_sum = ws.sum()

ew_mean = np.convolve(a, ws)[winSize - 1] / w_sum

bias = (w_sum ** 2) / ((w_sum ** 2) - (ws ** 2).sum())

ew_var = (np.convolve((a - ew_mean) ** 2, ws)[winSize - 1] / w_sum) * bias

ew_std = np.sqrt(ew_var)

return (ew_mean, ew_var, ew_std)

Дано alpha а также windowSizeВот подход для моделирования соответствующего поведения на NumPy:

def numpy_ewm_alpha(a, alpha, windowSize):

wghts = (1-alpha)**np.arange(windowSize)

wghts /= wghts.sum()

out = np.full(df.shape[0],np.nan)

out[windowSize-1:] = np.convolve(a,wghts,'valid')

return out

Образцы прогонов для проверки -

In [54]: alpha = 0.55

...: windowSize = 20

...:

In [55]: df = pd.DataFrame(np.random.randint(2,9,(100)))

In [56]: out0 = df.ewm(alpha = alpha, min_periods=windowSize).mean().as_matrix().ravel()

...: out1 = numpy_ewm_alpha(df.values.ravel(), alpha = alpha, windowSize = windowSize)

...: print "Max. error : " + str(np.nanmax(np.abs(out0 - out1)))

...:

Max. error : 5.10531254605e-07

In [57]: alpha = 0.75

...: windowSize = 30

...:

In [58]: out0 = df.ewm(alpha = alpha, min_periods=windowSize).mean().as_matrix().ravel()

...: out1 = numpy_ewm_alpha(df.values.ravel(), alpha = alpha, windowSize = windowSize)

...: print "Max. error : " + str(np.nanmax(np.abs(out0 - out1)))

Max. error : 8.881784197e-16

Испытание во время выполнения на большом наборе данных -

In [61]: alpha = 0.55

...: windowSize = 20

...:

In [62]: df = pd.DataFrame(np.random.randint(2,9,(10000)))

In [63]: %timeit df.ewm(alpha = alpha, min_periods=windowSize).mean()

1000 loops, best of 3: 851 µs per loop

In [64]: %timeit numpy_ewm_alpha(df.values.ravel(), alpha = alpha, windowSize = windowSize)

1000 loops, best of 3: 204 µs per loop

Дальнейшее повышение

Для дальнейшего повышения производительности мы могли бы избежать инициализации с помощью NaN и вместо этого использовать массив, выведенный из np.convolve, вот так -

def numpy_ewm_alpha_v2(a, alpha, windowSize):

wghts = (1-alpha)**np.arange(windowSize)

wghts /= wghts.sum()

out = np.convolve(a,wghts)

out[:windowSize-1] = np.nan

return out[:a.size]

Сроки -

In [117]: alpha = 0.55

...: windowSize = 20

...:

In [118]: df = pd.DataFrame(np.random.randint(2,9,(10000)))

In [119]: %timeit numpy_ewm_alpha(df.values.ravel(), alpha = alpha, windowSize = windowSize)

1000 loops, best of 3: 204 µs per loop

In [120]: %timeit numpy_ewm_alpha_v2(df.values.ravel(), alpha = alpha, windowSize = windowSize)

10000 loops, best of 3: 195 µs per loop

Вот еще одно решение, которое O придумала тем временем. Это примерно в четыре раза быстрее, чем решение панд.

def numpy_ewma(data, window):

returnArray = np.empty((data.shape[0]))

returnArray.fill(np.nan)

e = data[0]

alpha = 2 / float(window + 1)

for s in range(data.shape[0]):

e = ((data[s]-e) *alpha ) + e

returnArray[s] = e

return returnArray

Я использовал эту формулу в качестве отправной точки. Я уверен, что это можно улучшить еще больше, но это, по крайней мере, отправная точка.

@ Ответ Дивакара, кажется, вызывает переполнение при работе с

numpy_ewma_vectorized(np.random.random(500000), 10)

То, что я использовал, это:

def EMA(input, time_period=10): # For time period = 10

t_ = time_period - 1

ema = np.zeros_like(input,dtype=float)

multiplier = 2.0 / (time_period + 1)

#multiplier = 1 - multiplier

for i in range(len(input)):

# Special Case

if i > t_:

ema[i] = (input[i] - ema[i-1]) * multiplier + ema[i-1]

else:

ema[i] = np.mean(input[:i+1])

return ema

Однако это намного медленнее, чем решение для панды:

from pandas import ewma as pd_ema

def EMA_fast(X, time_period = 10):

out = pd_ema(X, span=time_period, min_periods=time_period)

out[:time_period-1] = np.cumsum(X[:time_period-1]) / np.asarray(range(1,time_period))

return out

Вывод:

Реализация:

def ema(p:np.ndarray, a:float) -> np.ndarray:

o = np.empty(p.shape, p.dtype)

# (1-α)^0, (1-α)^1, (1-α)^2, ..., (1-α)^n

np.power(1.0 - a, np.arange(0.0, p.shape[0], 1.0, p.dtype), o)

# α*P0, α*P1, α*P2, ..., α*Pn

np.multiply(a, p, p)

# α*P0/(1-α)^0, α*P1/(1-α)^1, α*P2/(1-α)^2, ..., α*Pn/(1-α)^n

np.divide(p, o, p)

# α*P0/(1-α)^0, α*P0/(1-α)^0 + α*P1/(1-α)^1, ...

np.cumsum(p, out=p)

# (α*P0/(1-α)^0)*(1-α)^0, (α*P0/(1-α)^0 + α*P1/(1-α)^1)*(1-α)^1, ...

np.multiply(p, o, o)

return o

Примечание: ввод будет перезаписан.

Благодаря решению @Divakar, и это действительно быстро. Тем не менее, это вызывает проблему переполнения, на которую указал @Danny. Функция не возвращает правильных ответов, когда длина больше 13835 или около того на моем конце.

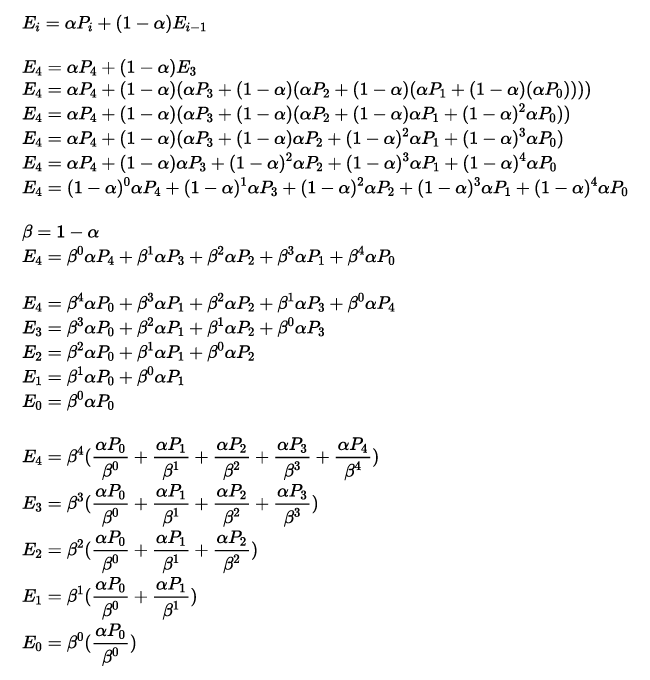

Следующее - мое решение, основанное на решении Дивакара и pandas.ewm(). Mean().

def numpy_ema(data, com=None, span=None, halflife=None, alpha=None):

"""Summary

Calculate ema with automatically-generated alpha. Weight of past effect

decreases as the length of window increasing.

# these functions reproduce the pandas result when the flag adjust=False is set.

References:

https://stackru.com/questions/42869495/numpy-version-of-exponential-weighted-moving-average-equivalent-to-pandas-ewm

Args:

data (TYPE): Description

com (float, optional): Specify decay in terms of center of mass, alpha=1/(1+com), for com>=0

span (float, optional): Specify decay in terms of span, alpha=2/(span+1), for span>=1

halflife (float, optional): Specify decay in terms of half-life, alpha=1-exp(log(0.5)/halflife), for halflife>0

alpha (float, optional): Specify smoothing factor alpha directly, 0<alpha<=1

Returns:

TYPE: Description

Raises:

ValueError: Description

"""

n_input = sum(map(bool, [com, span, halflife, alpha]))

if n_input != 1:

raise ValueError(

'com, span, halflife, and alpha are mutually exclusive')

nrow = data.shape[0]

if np.isnan(data).any() or (nrow > 13835) or (data.ndim == 2):

df = pd.DataFrame(data)

df_ewm = df.ewm(com=com, span=span, halflife=halflife,

alpha=alpha, adjust=False)

out = df_ewm.mean().values.squeeze()

else:

if com:

alpha = 1 / (1 + com)

elif span:

alpha = 2 / (span + 1.0)

elif halflife:

alpha = 1 - np.exp(np.log(0.5) / halflife)

alpha_rev = 1 - alpha

pows = alpha_rev**(np.arange(nrow + 1))

scale_arr = 1 / pows[:-1]

offset = data[0] * pows[1:]

pw0 = alpha * alpha_rev**(nrow - 1)

mult = data * pw0 * scale_arr

cumsums = np.cumsum(mult)

out = offset + cumsums * scale_arr[::-1]

return out

Разве экспоненциальный фильтр не то же самое, что БИХ-фильтр первого порядка? Почему бы вам не попробовать это:

from scipy import signal

signal.lfilter([alpha], [1, alpha-1], data)

где альфа варьируется от 0 до 1

Вот моя реализация для одномерных входных массивов с бесконечным размером окна. Поскольку он использует большие числа, он работает только с входными массивами с элементами с абсолютным значением < 1e16, когда используется float32, но это обычно должно иметь место.

Идея состоит в том, чтобы преобразовать входной массив в срезы ограниченной длины, чтобы не происходило переполнение, а затем выполнить вычисление ewm для каждого среза отдельно.

def ewm(x, alpha):

"""

Returns the exponentially weighted mean y of a numpy array x with scaling factor alpha

y[0] = x[0]

y[j] = (1. - alpha) * y[j-1] + alpha * x[j], for j > 0

x -- 1D numpy array

alpha -- float

"""

n = int(-100. / np.log(1.-alpha)) # Makes sure that the first and last elements in f are very big and very small (about 1e22 and 1e-22)

f = np.exp(np.arange(1-n, n, 2) * (0.5 * np.log(1. - alpha))) # Scaling factor for each slice

tmp = (np.resize(x, ((len(x) + n - 1) // n, n)) / f * alpha).cumsum(axis=1) * f # Get ewm for each slice of length n

# Add the last value of each previous slice to the next slice with corresponding scaling factor f and return result

return np.resize(tmp + np.tensordot(np.append(x[0], np.roll(tmp.T[n-1], 1)[1:]), f * ((1. - alpha) / f[0]), axes=0), len(x))

Все приведенные ниже ответы не учитывают отсутствующие значения, поэтому я даю свою версию, которая предполагает, что nan, а результат соответствует pandas EWM. Я использую numba для ускорения, и это в десять раз быстрее, чем реализация pandas.

matrix = df.values

@jit(nopython=True, nogil=True, parallel=True)

def ewm_mean(arr_in, com):

'''

calculate the exponential moving average for each column

$y_{t}=\frac{ewm_t}{w_t}$

$ewm_t = ewm_{t-1} (1 - \alpha) + x_t$

$w_t = w_{t-1} (1 - \alpha) + 1$

arr_in->ndarray(dtype=float64): ewm per column

com->int: $\alpha = 1/com + 1$

'''

t, m = arr_in.shape

ewma = np.empty((t, m), dtype=float32)

alpha = 1 / (com + 1)

# the size of blocks depending on the device, number of blocks should match the number of cores on your machine

sizeOfblock = 1000

numberOfblock = m // sizeOfblock

assert sizeOfblock*numberOfblock == m, "wrong split"

# main loop

for nb in prange(numberOfblock): # split columns to blocks

w = np.where(np.isnan(arr_in[0, nb*sizeOfblock: (nb+1)*sizeOfblock]), 0., 1.)

ewma_old = arr_in[0, nb*sizeOfblock: (nb+1)*sizeOfblock]

ewma[0, nb*sizeOfblock: (nb+1)*sizeOfblock] = ewma_old

for i in range(1, t): # accumulate row by row

data_now = arr_in[i, nb*sizeOfblock: (nb+1)*sizeOfblock]

ewma_old = np.where(np.isnan(ewma_old), 0., ewma_old)*(1-alpha) + data_now

if np.isnan(np.sum(data_now)): # check nan

nan_pos = np.isnan(data_now)

w = w * (1 - alpha) + np.where(nan_pos, 0., 1.)

d = ewma_old / w

ewma[i, nb*sizeOfblock: (nb+1)*sizeOfblock] = np.where(nan_pos, ewma[i-1, nb*sizeOfblock: (nb+1)*sizeOfblock], d)

else:

w = w * (1 - alpha) + 1.

d = ewma_old / w

ewma[i, nb*sizeOfblock: (nb+1)*sizeOfblock] = d

return ewma

np.isclose(df.ewm(com=2).mean().values, ewm_mean(matrix, com=2), equal_nan=True).all()

Набор данных выглядит так.

import pandas as pd

import numpy as np

np.random.seed(0)

df = pd.DataFrame(np.random.normal(0, 10, size=(4000, 5000)))

df.iloc[0:800, 1000:2000] = np.nan

df.iloc[800:1600, 2000:3000] = np.nan

df.iloc[1600:2400, 3000:4000] = np.nan

df.iloc[2400:3200, 4000:5000] = np.nan

Примечание. В этом коде много времени уходит на обработку чисел nan, поэтому я разбиваю данные на блоки и выполняю вычисления параллельно. Если ваши данные не имеют значений nan, вы можете внести незначительные изменения и значительно ускорить их. Кроме того, вы можете написать более сложную логику для назначения данных ядрам.

sizeOfblock- параметр; играть с этим.

Основываясь на великолепном ответе Дивакара, вот реализация, которая соответствует adjust=True флаг функции панд, то есть использование весов, а не рекурсии.

def numpy_ewma(data, window):

alpha = 2 /(window + 1.0)

scale = 1/(1-alpha)

n = data.shape[0]

scale_arr = (1-alpha)**(-1*np.arange(n))

weights = (1-alpha)**np.arange(n)

pw0 = (1-alpha)**(n-1)

mult = data*pw0*scale_arr

cumsums = mult.cumsum()

out = cumsums*scale_arr[::-1] / weights.cumsum()

return out